Thinking about giving your kitchen a new look in 2024? Figuring out how to pay for it can be a big part of the plan. That’s where kitchen remodel financing comes in. This article will help you understand your options in simple terms, so you can make the best choice for your budget and your dream kitchen.

What is Kitchen Remodel Financing?

First things first, what do we mean by kitchen remodel financing? It’s just a fancy way of finding the money to pay for your kitchen makeover. There are a few different ways to do this, like getting a loan or using a credit card. We’ll look at these options so you can pick what works best for you.

Popular Ways to Finance Your Kitchen Remodel

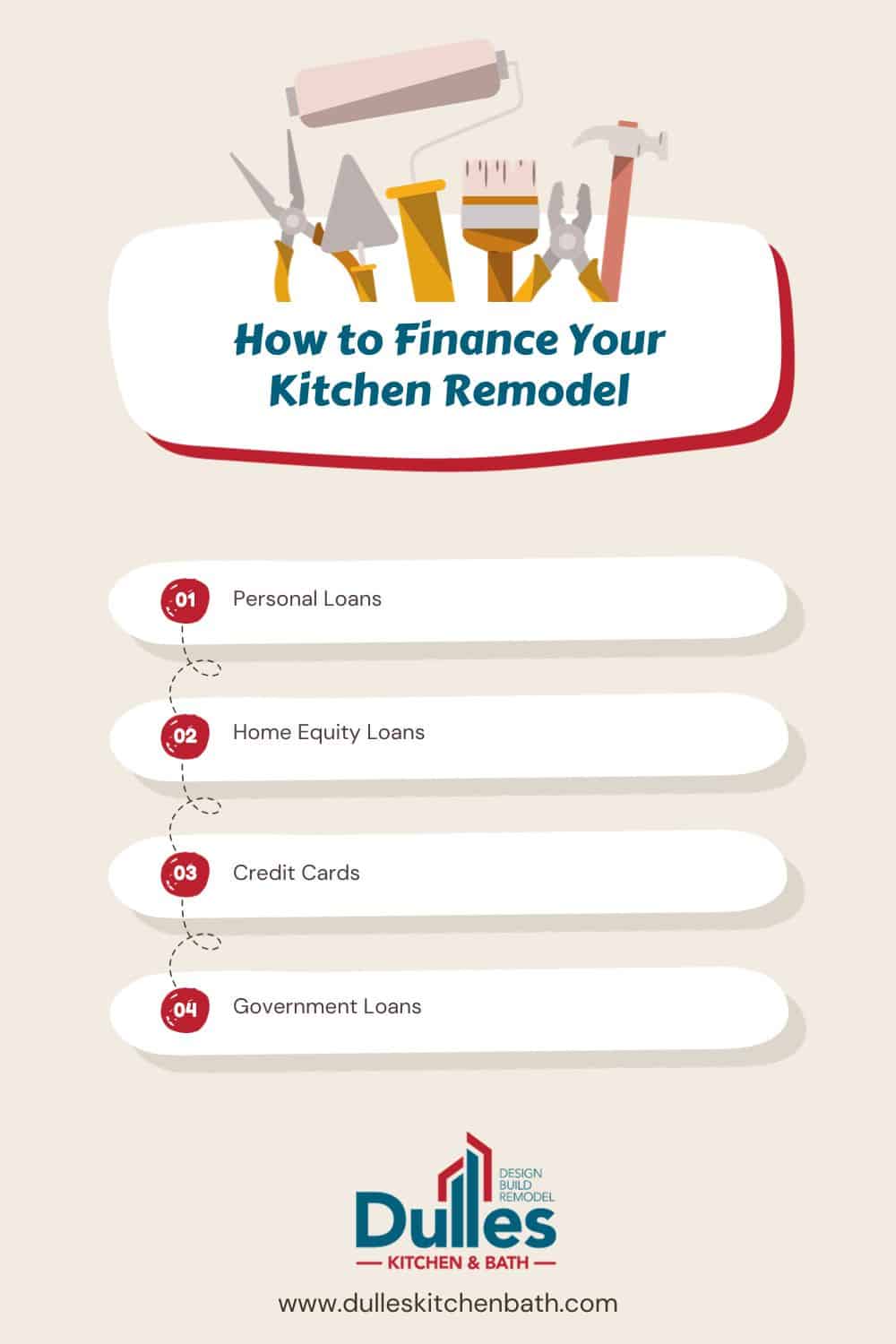

1. Personal Loans

Personal loans are a handy way to get money from banks or online lenders, especially if you need cash fast for your kitchen redo. They’re great because you don’t need to promise your house or other stuff you own as a backup for the loan. This is good news if you don’t want to risk losing your things. The flip side is that the interest (the extra money you pay back on top of the loan) might be a bit higher since you’re not offering anything as backup. Getting a personal loan is usually easy, and some places might even say yes to your loan in just a few days. So, if you want money quickly and don’t want the hassle of linking your loan to your house, personal loans are a solid choice.

2. Home Equity Loans

Home equity loans are really useful for people who have paid off a big part of their house. Think of equity as the part of your house you actually own. It’s what your house is worth minus what you still owe on your mortgage. When you get a home equity loan, you’re basically borrowing money against the part of your house you own. A big plus of this kind of loan is that the interest rates (the extra money you pay back) are usually lower because your house is used as security for the loan. This means the monthly payments can be more manageable than other loan types. It’s a smart choice if you’re planning a big, costly makeover for your kitchen. Just remember, there’s a catch: if you can’t keep up with the payments, you could risk losing your house.

3. Credit Cards

Credit cards offer a quick and accessible way to finance smaller kitchen remodels. Many homeowners opt for this route when they’re making minor updates or cosmetic changes. The application process is often simple, especially if you already have a card with a sufficient credit limit. The major caveat with credit cards is their high interest rates. If you don’t pay off the balance quickly, the interest can accumulate, making this a costly option in the long run. It’s best to use credit cards if you’re confident you can pay off the debt swiftly or if you have a card with a low-interest promotional period.

4. Government Loans

For those aiming to make their kitchens more energy-efficient, government loans can be an excellent resource. These loans are often offered at favorable terms to encourage homeowners to upgrade their kitchens in ways that reduce energy consumption. This might include installing energy-efficient appliances, better insulation, or more efficient windows. The specifics of these loans, including interest rates and terms, can vary depending on the program and where you live. It’s worth researching to see if you qualify for these incentives, especially if your remodel includes eco-friendly upgrades.

Check Your Budget First

Before you decide how to finance your kitchen remodel, take a good look at your finances. How much money do you have saved up? How much can you comfortably spend each month on loan payments? Answering these questions will help you choose the right financing option.

Choosing the Best Option for You

- Look at Interest Rates: Different loans have different rates, so shop around.

- Think About the Loan Term: This is how long you have to pay back the loan. Shorter terms usually mean higher monthly payments.

- Watch Out for Extra Fees: Some loans have fees for things like late payments, so make sure you know about these.

Conclusion

Financing your kitchen remodel in 2024 doesn’t have to be complicated. By understanding your options and what you can afford, you can make a smart choice that lets you create your dream kitchen without breaking the bank.

FAQ Section

What should I think about when picking a kitchen remodel loan?

Look at interest rates, how long you have to pay back the loan, and your current financial situation.

Are there loans just for kitchen remodeling?

Not specifically, but personal loans, home equity loans, and government loans are often used.

Can I use my credit card for a kitchen remodel?

Yes, for smaller projects. Just be careful of high-interest rates.